The Tax Cuts and Jobs Act of 2017 places some IP rights holders squarely in the sights of the tax collector, while providing others with an opportunity to license overseas without having to resort to international asset transfers to maximize returns.

Patent, trademark and copyright owners of all sizes would be wise to revisit the nature and tax implications of their transactions, including direct patent sales, as well as where their IP assets are best located. This is a direct result of the Tax Cuts and Jobs Act of 2017 (TCJA), the impact of which on IP holders is starting to be understood.

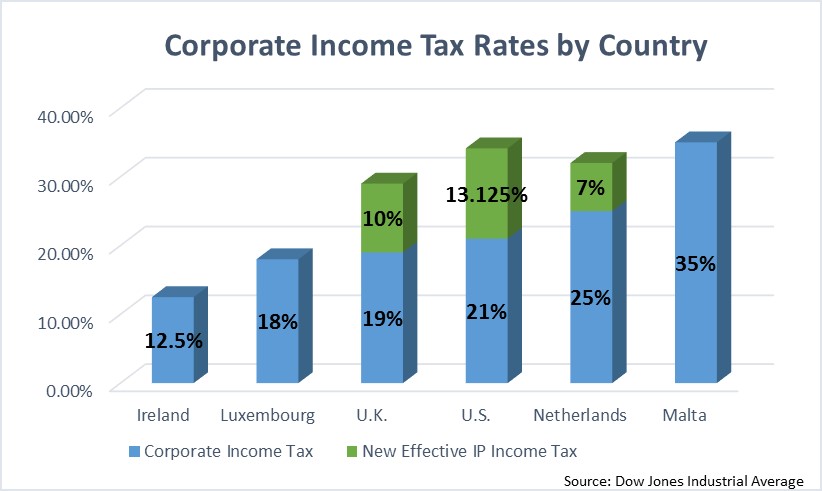

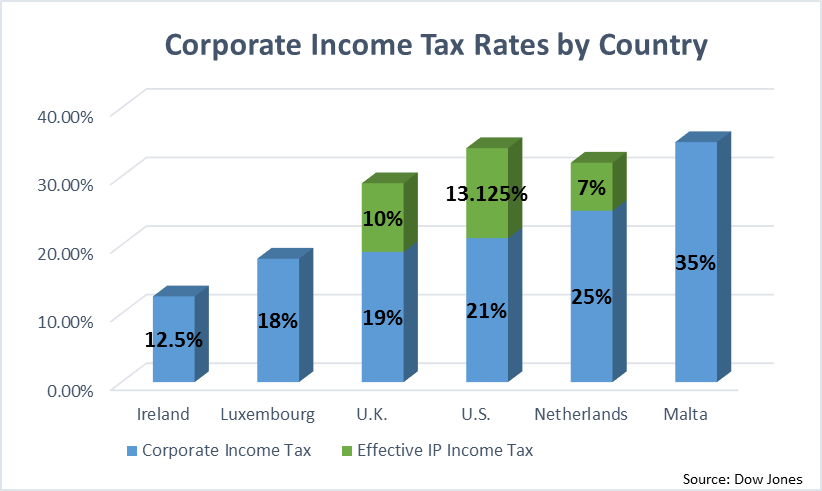

The new law is partly a response to businesses that hold massive amounts of revenue-producing assets outside the United States in so-called ‘patent boxes’ – devices which allow revenue on assets held within them to escape most local and all domestic taxes derived from IP-related revenue.

Like Wildfire

“Patent boxes have spread like wildfire,” Edward Kleinbard, former chief of staff of the US Congress’s Joint Committee on Taxation, now a law professor at the University of Southern California told the Intangible Investor. “Their success was doomed from the start. The international environment for intangibles and tax has evolved. With more products to license from sources worldwide and more revenue derived from them, these devices, which originally were restricted to a handful of nations, have become diffuse.”

The most famous (or infamous) product of the IP asset tax avoidance schemes, known as the “double Irish,” has been used by large corporations, including Facebook Inc, Google parent Alphabet, Inc and drug maker Allergan PLC.

The TCJA aims to lure IP locations back to the US, but whether the benefits are sufficiently attractive is still unclear. The Wall Street Journal coverage of the TCJA can be found here. For the American Enterprise Institute take on the Act, go here.

Rana Foroohar, a journalist who reports for the Financial Times, says in a video that a growing “tech-lash” (backlash) against the imbalance of power generated by U.S. tech giants extends to how they use proceeds from overseas licensing revenues to buy foreign bonds. Curtailing this activity has the potential to cause disruption in the bond market and interest rates, she says. Foroohar’s video clip on the potential ramifications of tax increases can be found here.

Self-Licensing

Rather than licensing to themselves (or the entities they control) to generate income that avoids taxes and use those proceeds to invest in corporate bonds, techcos might consider generating genuine IP revenues, as well as taking, and paying for, licenses they need from other holders.

For the full Intangible Investor story, “Identifying the impact of the US tax act,” in the May IAM magazine out this week, go here.

Image source: brodyberman.com