Publicly traded patent licensing companies have significantly under-performed market indexes. Only a few of the original listed stocks remain.

The IP CloseUp 30, a feature of this blog first published in 2013, was designed to provide IP investors a real-time snapshot of public patent licensing company performance and news.

Loss of patent certainty and value have made licensing less interesting to current equity investors. For that reason, the IP CloseUp 30 is evolving. It will be known as the IP CloseUp 50, and include several new categories of publicly traded, IP-focused businesses, including those that engage in brand and content licensing and defensive strategies.

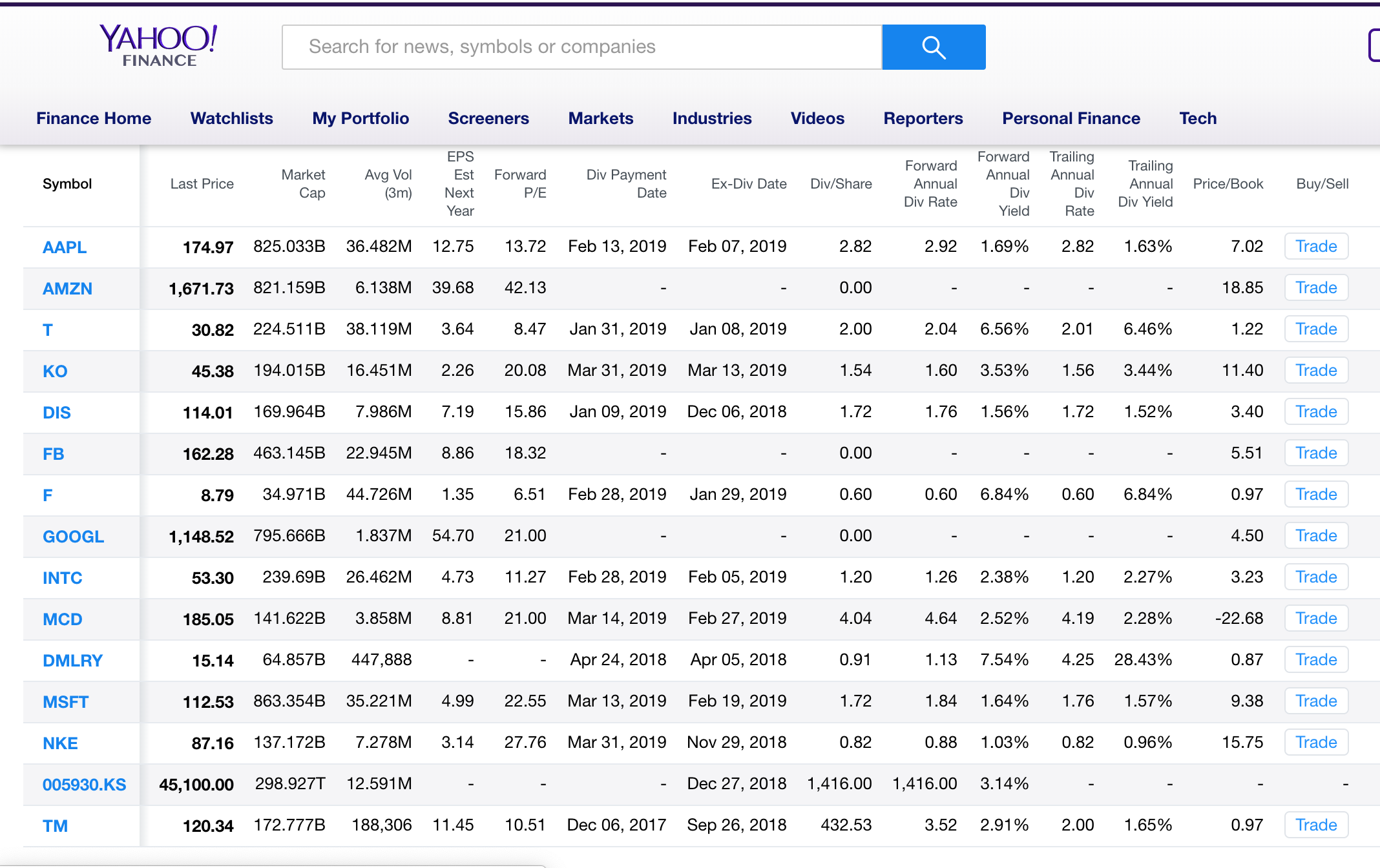

The IP CloseUp 30 index is build on a Yahoo! Finance screen of earnings and other financial information — stock price and market capitalization, as well as real-time news developments. It gives IP investors a efficient way to track relative performance of selected companies. For those observers more dubious about the sector, but who are interested in keeping tabs on certain patent holders, it provides a method of tracking potential threats.

Evolving Universe

When I coined the acronym, PIPCO, six years ago, it referred to an expanding sector of public companies whose primary source of revenue was patent licensing and, by default, litigation. At the time patent values and damages were much higher and many respectable non-practicing entities (NPEs) held promise. Yet to be felt were the full impact of the America Invents Act, passed in 2012, and the effects of several major court decisions affecting injunctive relief and patent eligibility.

Leading Brands Category

The IP CloseUp 50 is an alternative method for investors to track the influence if not impact of intellectual property. It introduces a larger context for considering IP performance. Patent monetization remains a viable business model for some owners, but perhaps for most businesses, less so as a public one with the pressure to provide investors with quarterly results.

The IPCU 50 is far from definitive and will require that companies be added and removed as market and IP conditions warrant. PIPCOs were never intended to be just about patent licensing. When damages awards for mobile telephony (Motorola, Nortel, et al.) and other technologies commanded hundreds of millions if not billions of dollars, it was only natural for licensing companies to become a source or investor fascination. But even at their most active these PIPCOs rarely generated much daily volume or market capitalization.

Enter PIPCO 2.0

If investors have learned one thing over the past decade about public IP companies it is that they are not synonymous with patent licensing. It is true that performance measures like licensing, settlements and public awards are easier to follow than return on risk mitigation or brand equity. Licensing and litigation are simply more graphic, especially if big tech companies are paying out.

Think of the IPCU 50 as IP CloseUp 2.0. It represents the next iteration of IP investment perspective – companies better equipped to adapt and survive because of their nature of their IP assets and their size. It includes patent, trademark and content-focused operating businesses where licensing may play a role in performance. The index will still consider leading patent licensing companies, but scale back the number. (For now, the index will not consider trade secrets directly.)

To be sure, the IPCU 50 is a work in progress, destined to be refined, but, nonetheless, provocative and worthy of periodic scrutiny.

The new IP CloseUp 50 categories:

- Patents – Technology

- Patents – Pharmaceuticals

- Trademarks – Leading Brands

- Media & Content Owners (Copyright)

- Primarily Patent Licensing

Fuller Grasp

Using IP rights to mitigate risk and maintain market share is not new. Nor is brand or content licensing. In principle, using IP rights defensively does not necessarily diminish their significance. It is true that specific tech patents typically mean more to small businesses and individuals than to established players who can rely on other resources like brand equity and their ability to raise capital, and are unlikely to enforce infringed patents. A fuller grasp of what different types of IP mean to various businesses can quickly turn a seller into a buyer (and vice versa).

With some 85% or more of S&P 500 company value tied up in intangibles assets such as IP rights, shareholders need to be better informed about the use of and return on IP (call it, ROIP) and their role in performance. Questions investors should be asking, even if senior management and equity analysts are reluctant to:

- Which are the most IP-rich businesses?

- What rights do they own?

- How are they being used?

- What is the relationship of their IP to performance and shareholder value?

Work in Progress

To be meaningful the IP CloseUp 50 must change to reflect IP value and investor need. The businesses were initially selected by an informal panel of experts. We will do our best to accommodate requests to add or delete companies. The index is designed to render performance of IP-rich companies somewhat more transparent and easier to follow.

The IP CloseUp 50 looks at top public IP holders primarily by:

- Size, type and quality of IP portfolio and assets

- Enterprise market value (typically >$500M)

- Innovation reputation

For further explanation of the five sections and criteria for inclusion, visit the IP CloseUp 50 landing page, here. Consider bookmarking it or placing it on your home screen or desktop.

Image source: yahoo! finance; ipcloseup.com

One comment